The Canadian market has been experiencing a positive trend, with the TSX reaching all-time highs, buoyed by optimism surrounding central bank policies and strong corporate earnings. In this environment of economic expansion and rising valuations, high-growth tech stocks in Canada present intriguing opportunities for investors seeking to capitalize on innovation and technological advancements.

Top 10 High Growth Tech Companies In Canada

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Docebo | 14.71% | 33.96% | ★★★★★☆ |

| Constellation Software | 16.17% | 23.55% | ★★★★★☆ |

| HIVE Digital Technologies | 48.71% | 94.27% | ★★★★★☆ |

| GameSquare Holdings | 38.08% | 86.64% | ★★★★★☆ |

| Blackline Safety | 22.29% | 121.23% | ★★★★★☆ |

| Medicenna Therapeutics | 62.37% | 57.20% | ★★★★★☆ |

| Cineplex | 7.22% | 179.27% | ★★★★☆☆ |

| BlackBerry | 24.19% | 79.50% | ★★★★★☆ |

| Alpha Cognition | 62.98% | 69.54% | ★★★★★☆ |

| Sernova | 76.56% | 74.04% | ★★★★★☆ |

Click here to see the full list of 24 stocks from our TSX High Growth Tech and AI Stocks screener.

Let’s dive into some prime choices out of from the screener.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Computer Modelling Group Ltd. is a software and consulting technology company that develops and licenses reservoir simulation and seismic interpretation software, with a market cap of CA$910.19 million.

Operations: CMG generates revenue primarily from the development and licensing of reservoir simulation and seismic interpretation software, amounting to CA$90.29 million. The company operates within the software and consulting technology sector, focusing on providing specialized solutions for reservoir management.

Computer Modelling Group Ltd. (CMG) is navigating the high-growth tech landscape in Canada with a strategic focus on innovation and market expansion, evidenced by its recent product launch and index inclusion. The company’s R&D expenditure has been pivotal, maintaining a robust pipeline of advanced simulation tools like the newly launched Focus CCS, which enhances CO2 storage site selection—a critical component in combating climate change. CMG’s financial trajectory reflects an anticipated earnings growth of 24.6% annually, outpacing the Canadian market projection of 14.6%. Despite a challenging environment with profit margins receding to 19.7% from last year’s 29.2%, CMG’s revenue is expected to climb by 11.5% yearly, signaling resilience and adaptability in its operational strategy.

Recent developments underscore CMG’s commitment to maintaining its competitive edge and addressing global sustainability challenges. The addition to the S&P Global BMI Index marks a significant recognition of its market value and stability, while collaborations like with Sval Energi AS for the Trudvang project position it at the forefront of technological advancements in carbon capture and storage solutions—integral for future energy strategies globally.

Simply Wall St Growth Rating: ★★★★★☆

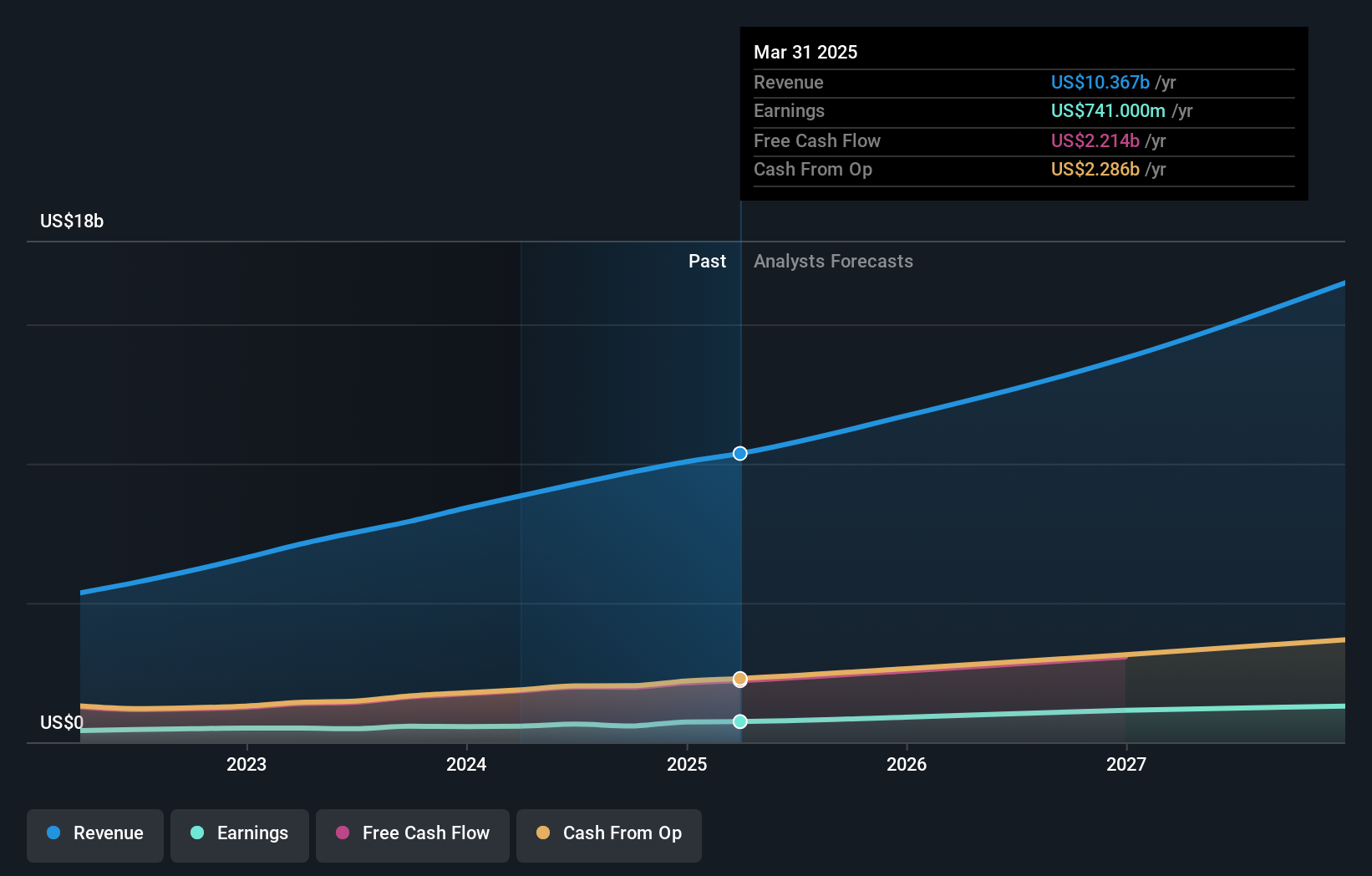

Overview: Constellation Software Inc. is a company that acquires, builds, and manages vertical market software businesses across Canada, the United States, Europe, and internationally, with a market cap of CA$92.18 billion.

Operations: Constellation Software focuses on acquiring and managing vertical market software businesses globally. Its primary revenue stream is from the Software & Programming segment, which generated $9.27 billion.

Constellation Software demonstrates robust growth in the tech sector, with a significant 23.6% expected annual earnings growth outpacing the Canadian market forecast of 14.6%. This performance is underpinned by a strong commitment to R&D, which has seen an increase in expenses, crucial for fostering innovation and maintaining competitive advantage in software development. Recent financials reveal a surge in revenue to USD 4.82 billion, up from USD 3.96 billion last year, coupled with net income rising to USD 282 million from USD 198 million. These figures underscore Constellation’s effective strategy and operational efficiency amidst evolving market demands. The company also supports shareholder value through consistent dividends, with the latest being $1 per share payable soon, reflecting its stable financial footing and confidence in sustained growth.

Simply Wall St Growth Rating: ★★★★☆☆

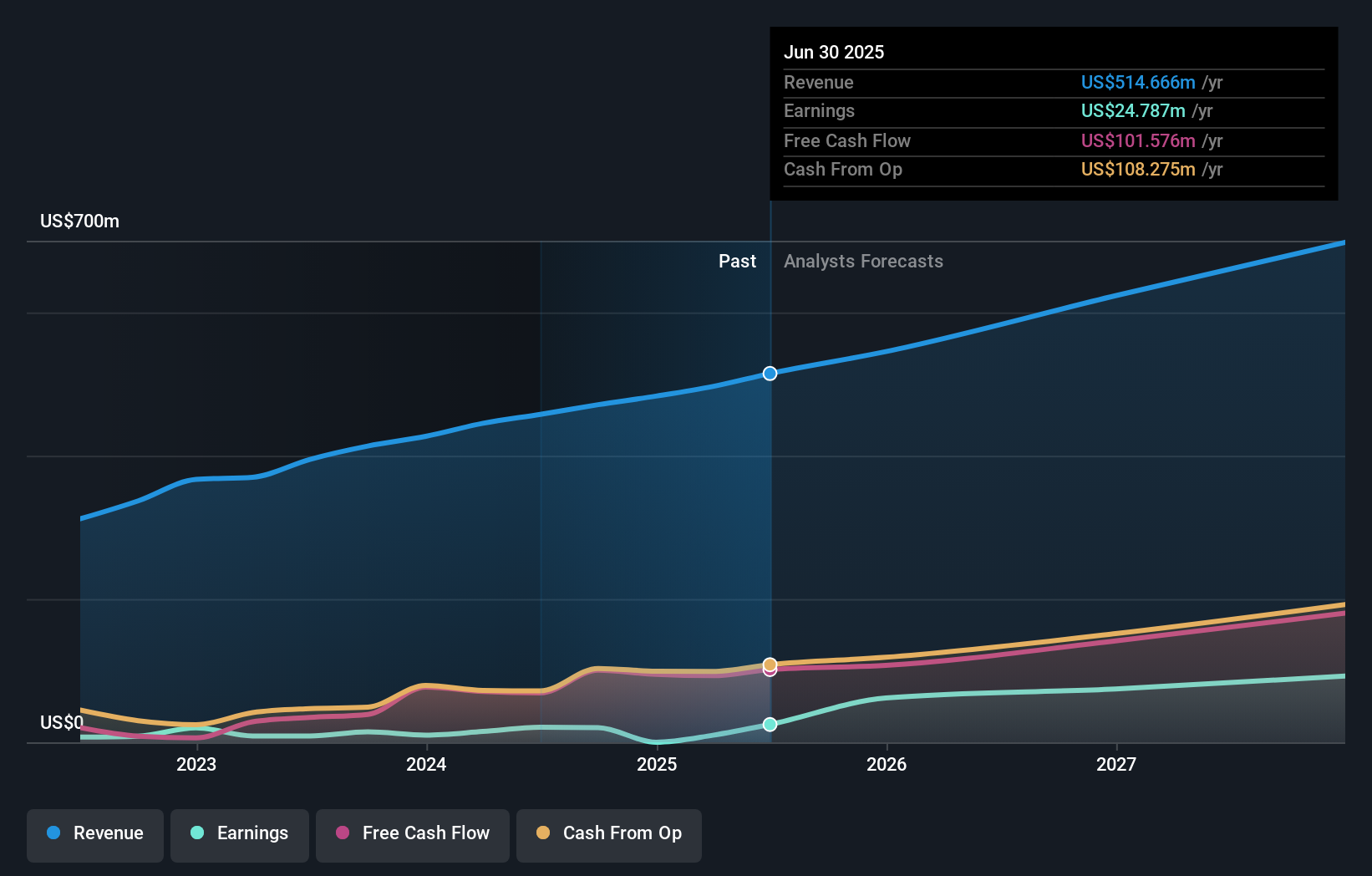

Overview: Kinaxis Inc. offers cloud-based subscription software focused on supply chain operations across the United States, Europe, Asia, and Canada with a market capitalization of CA$4.47 billion.

Operations: Kinaxis generates revenue primarily through its software and programming segment, amounting to $457.72 million. The company focuses on providing cloud-based solutions for supply chain management across various regions including the United States, Europe, Asia, and Canada.

Kinaxis, a leader in supply chain management software, is demonstrating robust growth with a forecasted revenue increase of 14.5% per year, outpacing the Canadian market average of 7%. This growth is complemented by an impressive expected annual earnings surge of 47%, highlighting the company’s operational efficiency and innovation in AI-powered solutions like its Maestro platform. Notably, Kinaxis has intensified its R&D efforts, dedicating significant resources to ensure continuous improvement and competitiveness in a complex industry. The recent strategic client addition of Mahindra & Mahindra Ltd., enhancing their auto supply chain capabilities with Kinaxis’ technology, underscores the company’s expanding influence and potential for sustained growth amidst market challenges.

Summing It All Up

Ready To Venture Into Other Investment Styles?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Kinaxis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com