{kind=link}

Key Points:

- Canadian job seekers faced difficult conditions to end 2024, as landing one’s first job, finding re-employment, and changing employers have all become tougher amid rising unemployment.

- Improvement in 2025 will depend on if the economy can generate stronger employer demand: Despite firming in Q4, job postings on Indeed were down 9% from a year earlier in December, which if continued could push the unemployment rate towards 7.5%.

- Employer hiring appetite has cooled across the board, but job postings are still elevated in many regions (like smaller cities and rural areas) and for several occupations (especially healthcare, but also, education, engineering, and certain white-collar jobs).

- Foreign job seeker interest in Canadian jobs has plunged in the wake of new policies aimed at slowing population growth, especially for job postings in certain low and mid-paying occupations, but to muted effect on the employer hiring environment amid the weaker overall labour market. The impacts from rising outflows of non-permanent residents will be a wildcard in 2025.

- Wage growth was surprisingly robust in 2024 but will likely ease, as catch-up in paychecks to the earlier jump in cost of living fades. Growth of advertised wages on Indeed job postings slowed to a 3.0% year-over-year pace by October 2024.

- The share of Canadian job postings mentioning generative AI doubled in 2024 but remained quite low outside of postings for tech-related jobs, highlighting the still-limited application of the technology across much of the economy.

With year-end approaching, the general verdict on the 2024 Canadian labour market is that it was “not good, but could have been worse.” So what does this mean for 2025?

It’s unlikely conditions will turn around quickly. The unemployment rate in November 2024 stood at 6.8%, not especially high by historical standards but trending in the wrong direction, up 1.0 percentage point from a year earlier. And the deterioration was quite steady throughout 2024, with job growth, according to the Labour Force Survey (LFS), lagging rapid population growth in all but two months. Joblessness hasn’t spiked as it did during previous downturns, mainly because layoff rates have been relatively low, but slow hiring has weighed substantially on the overall labour market.

The combination of slow hiring and low layoffs has created a growing divide in conditions facing Canadian workers. Solid job stability has benefited comfortably employed people not necessarily looking for a change, but the situation has deteriorated for job seekers across a range of circumstances:

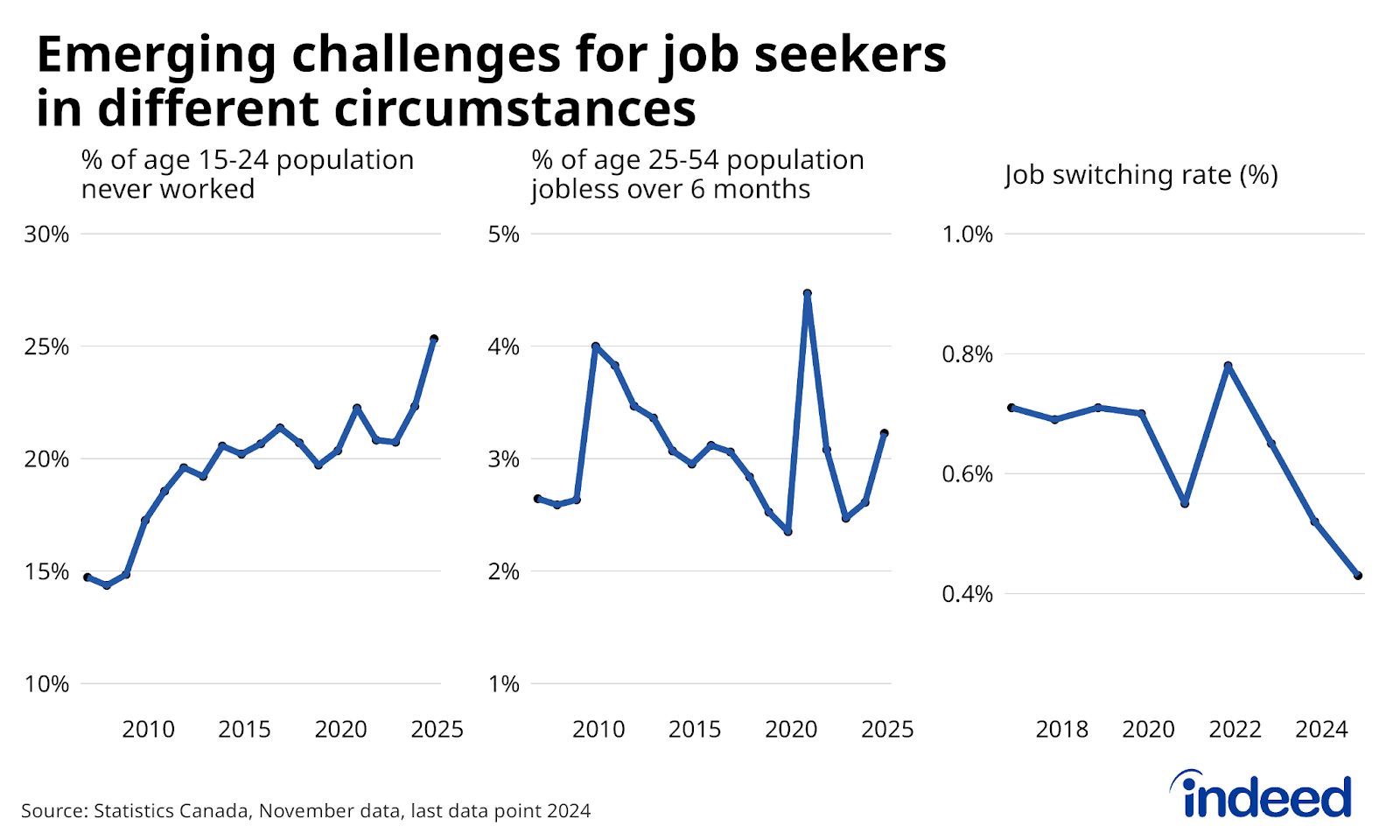

- Youth are finding it tougher to land their first jobs. In November 2024, 25% of 15-to-24-year-olds had never worked before, up noticeably from the 20%-21% November rates that prevailed from 2013 through 2021.

- It’s taking longer for out-of-work, core-age (25-to-54-year-old) Canadians to return to work. Long-term joblessness (those who want a job but haven’t worked in more than six months) isn’t particularly elevated, but rose from 2.5% in late 2022 to 3.2% in November 2024.

- Job hopping — a key way people advance their careers — is down sharply. Following a temporary upswing in 2021, the monthly job switching rate has trended lower. It was just 0.43% in November 2024, well below its 0.7% pre-pandemic average.

Stronger employer demand is crucial for a labour market turnaround

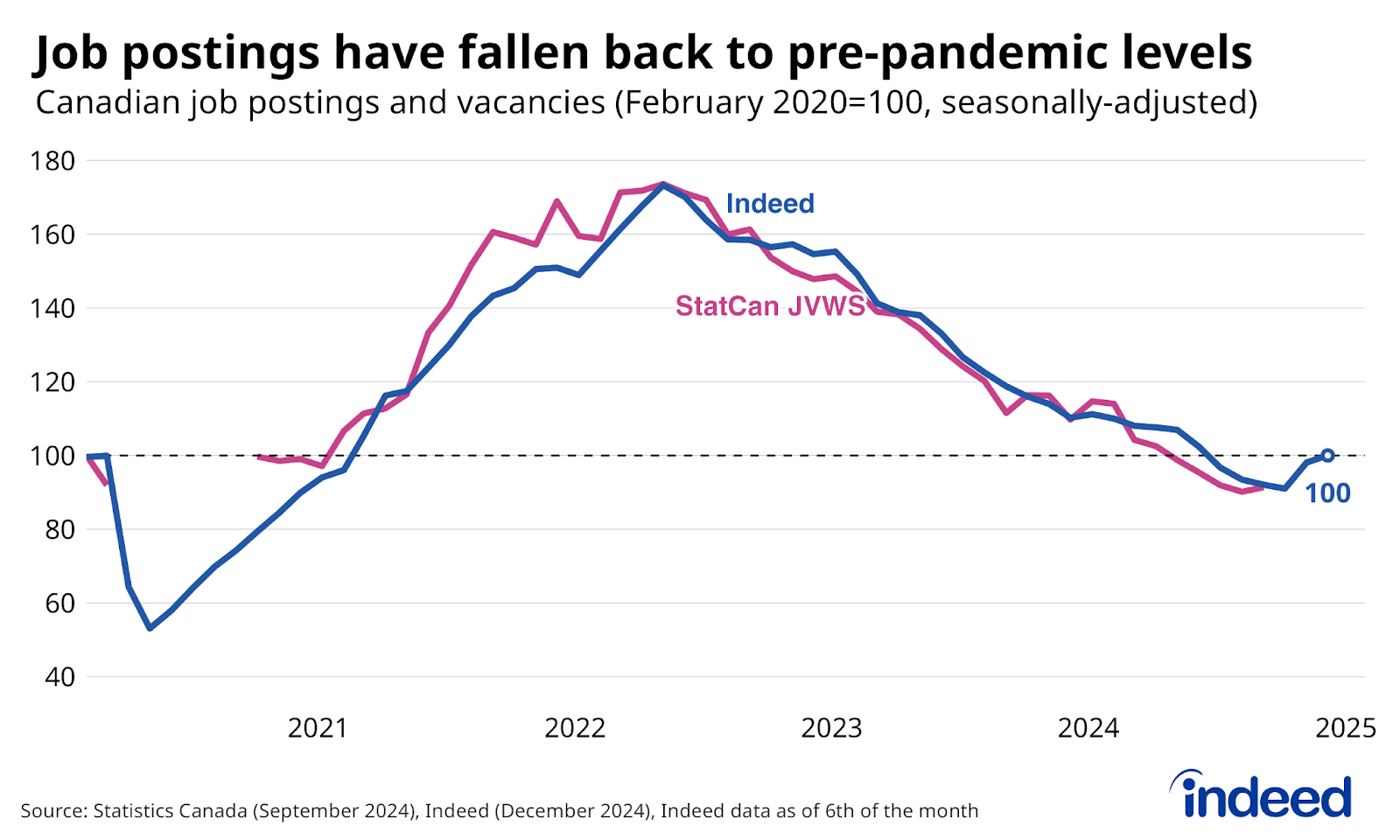

Employer demand will have to rebound, or at least stabilize, for job seeker conditions to improve in 2025. Total job postings on Indeed have moved higher since mid-September, but it’s too soon to call this uptick a trend. Canadian job postings still began December down 9% from a year earlier, matching their pre-pandemic level. Job vacancies, as measured by Statistics Canada’s Job Vacancy and Wage Survey (JVWS), were tracking similarly as Indeed postings through September, down 18% year-over-year.

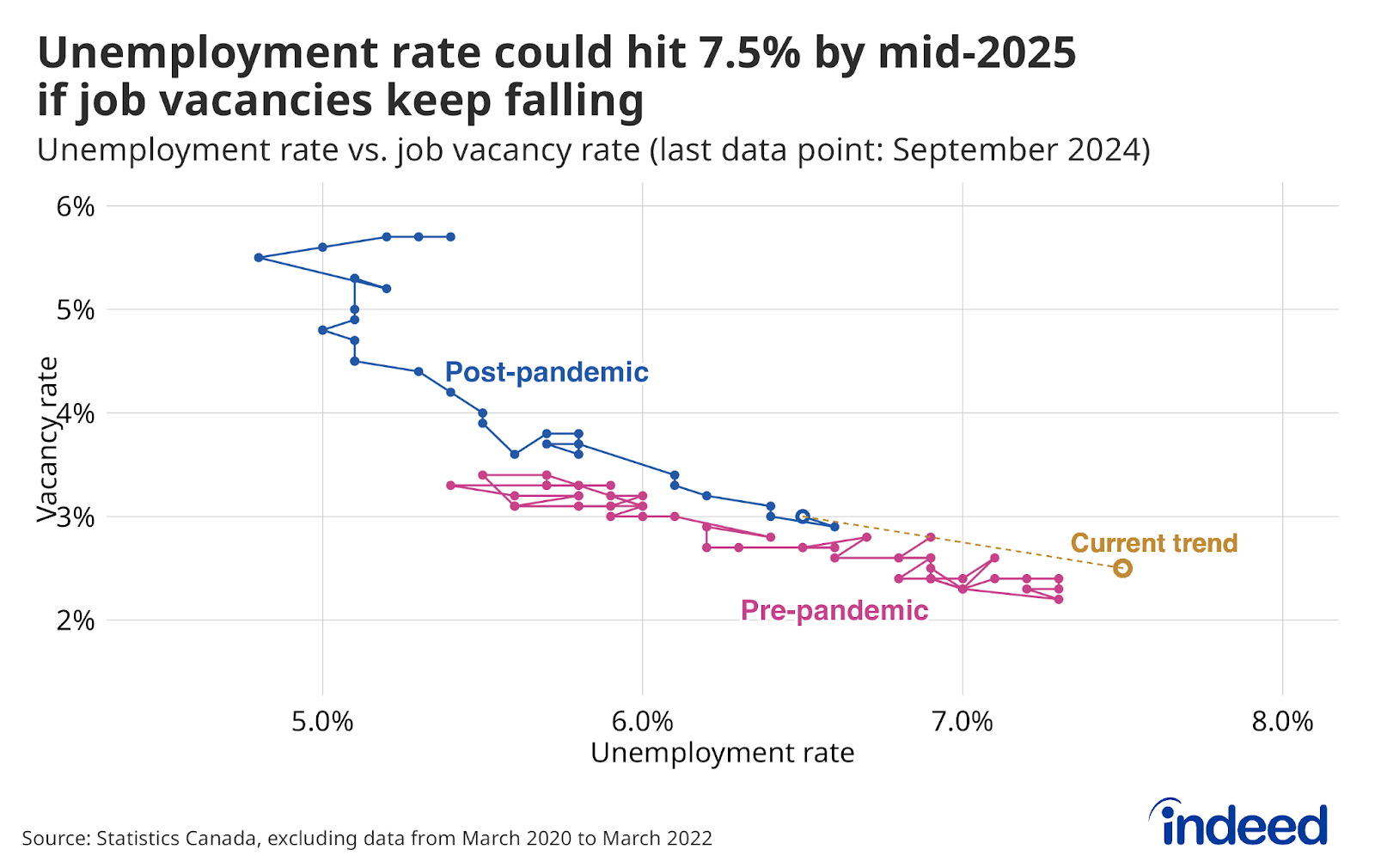

Further declines in job openings would likely spell significant trouble for the labour market. The historical relationship between job vacancies and unemployment (known as the “Beveridge Curve”) suggests that joblessness is currently more sensitive to changes in labour demand than when the labour market was tighter in 2023. All else equal, this means an additional 0.5-point drop of the vacancy rate from its current 3.0%, could easily coincide with the unemployment rate rising to 7.5%. However, the ultimate trajectory of employer demand will depend on the broader state of the economy.

Until recently, forecasts for 2025 projected a slight improvement in GDP growth ahead — partly because of the waning impacts of earlier Bank of Canada interest rate hikes — and a pick-up in per-capita GDP, after factoring in an expected slowdown in population growth. These developments would help avoid further labour market deterioration. Still, downside risks to the economy loom. One is that the factors currently weighing on growth persist, and the job market continues its gradual deterioration. However, things could also turn worse, particularly if layoffs rise amid uncertainty from a potential upheaval in Canada-US trade relations.

Demand for workers varies across different segments of the labour market

Taking a longer view of employer hiring appetite, the overall boom and subsequent decline in total job postings since early 2020 has been evident in postings across almost all sectors and regions. Nonetheless, the extent of the ups and downs varies widely, with opportunities for job seekers still relatively robust in some segments of the labour market, and quite weak in others.

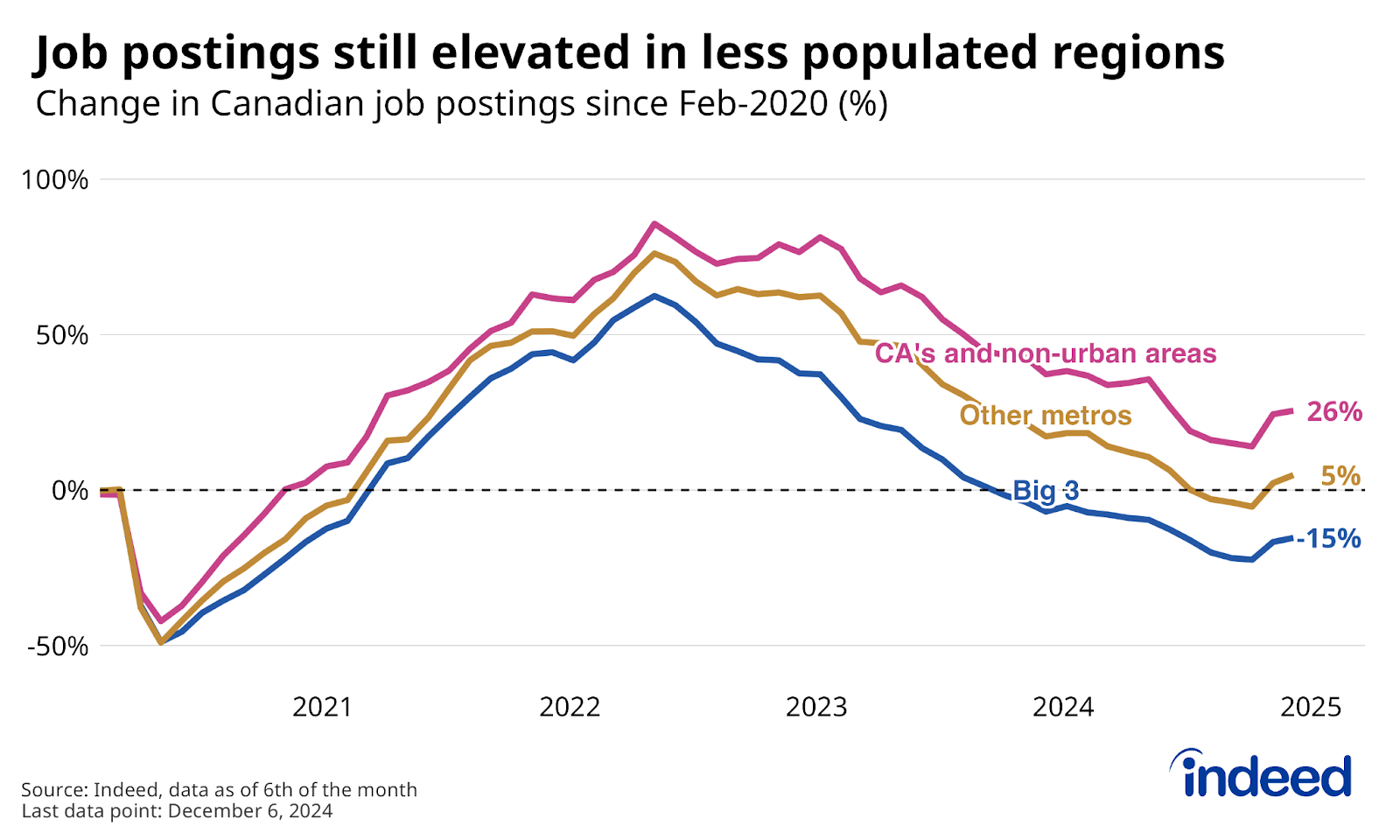

One of the dividing lines is across regions: Generally, the larger the population centre, the lower job postings stand compared to early 2020. Postings in Canada’s largest three metros started falling before other regions, and a gap has remained since. Taken together, on December 6, job ads in the Toronto, Montreal, and Vancouver areas were down 15% from their pre-pandemic level. Conversely, postings in non-metro areas, while also substantially lower than their peak, remained up 26%. Other metro areas were in between, up 5%, albeit weighed down by large declines in Ontario metros like Ottawa, Kitchener-Waterloo-Cambridge, and Hamilton.

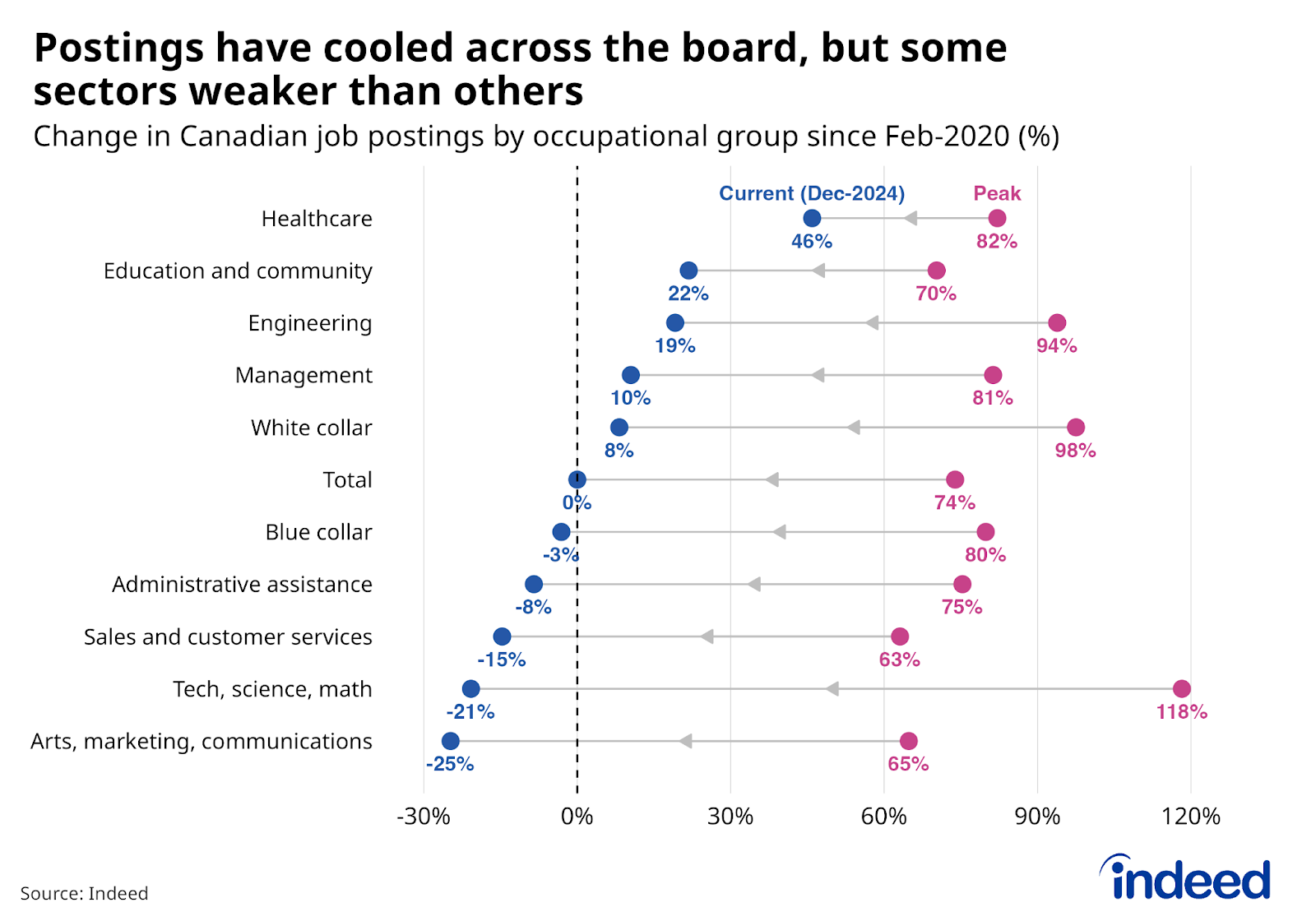

Contrasts are also evident between occupations. Grouping occupations tracked by Indeed into larger categories, postings across all major segments have retreated from their post-pandemic peaks. However, where they stand compared to early 2020 varies substantially. Healthcare stands out, with postings far above pre-pandemic levels, reflecting the sector’s unique hiring cycle. Meanwhile, despite having cooled sharply, demand is still up somewhat in higher-paying fields like engineering, management, and a range of white-collar occupations, like banking and finance, insurance, and legal services (though accounting and HR are somewhat weaker).

On the flip side, postings in several occupational groups are below pre-pandemic levels, but by different degrees. Openings for blue-collar roles are down slightly from February 2020, though within this category, some sectors are faring relatively well (installation and maintenance). Others, like construction, are close to their pre-pandemic level, while manufacturing, driving, and loading and stocking are down.

Hiring appetite has dropped more in sales and customer-facing services (including retail, though food services has been a tad stronger), as well as marketing and communications. Job postings in tech, science, and math are also well below early 2020 levels, but unlike today’s other relatively weak sectors, these fields experienced the greatest growth across all sectors during the 2021-2022 boom. Employer hiring appetite has cooled nearly universally since then, but conditions facing job seekers heading into 2025 are still different, depending on the types of jobs they’re looking for, and what region they’re looking in.

Immigration, and especially emigration, are key policy wildcards for the labour market

If recent policy announcements bear fruit, Canadian population growth is set to whiplash, from a record two-year pace, to a sudden standstill in 2025. The Federal Government’s planned reduction in future permanent residency admissions will play a role, but most of the shift is set to come from a plunge in non-permanent residents — including international students and workers with temporary work visas — who have been the main drivers of the recent increase.

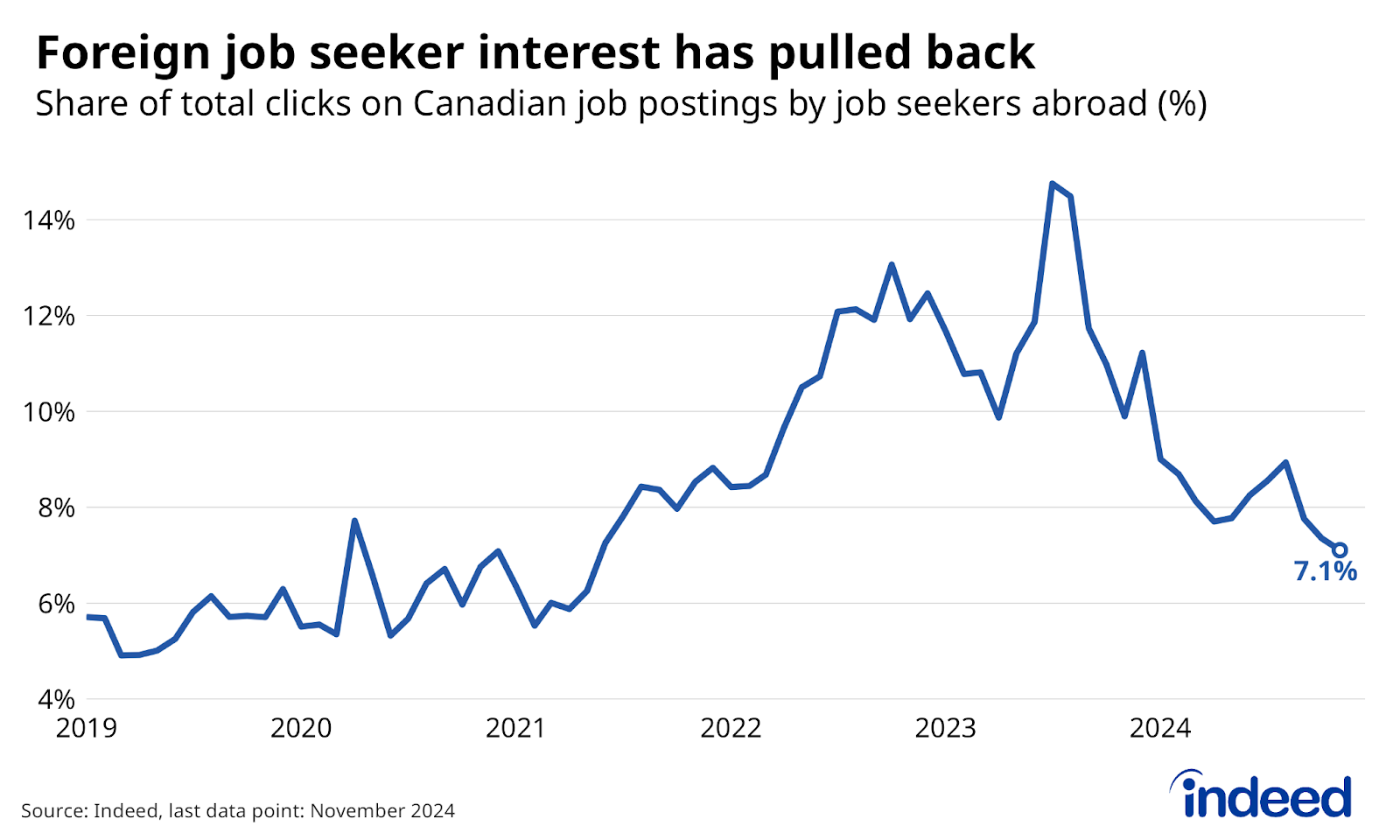

Migration to Canada started to slow in mid-2024, and Indeed data foreshadows a further shift to come. The environment has already changed substantially at the initial stage of the hiring process, when job seekers and employers connect on the Indeed platform. The share of clicks on Canadian job postings from abroad soared from about 6% of total clicks in early-2021, to more than 14% in mid-2023, but has since slid back to roughly 7% as of November 2024.

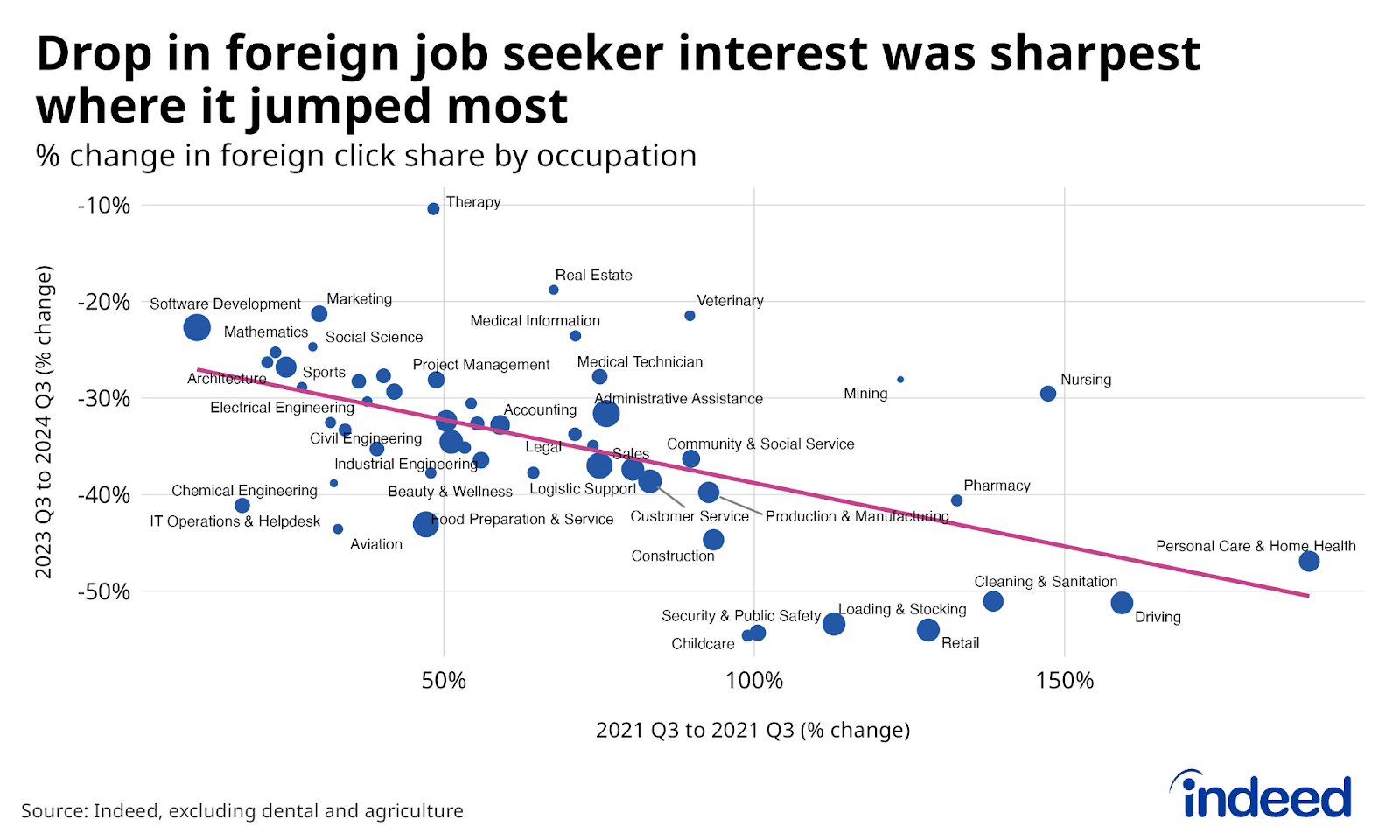

This rise and fall in foreign job seeker interest occurred across occupations. However, many of the sectors with fastest increases in foreign job seeker footprint between Q3 2021 and Q3 2023 — like personal and childcare, cleaning and sanitation, driving, and retail — have seen some of the sharpest declines in foreign click share since, several by more than half. A number of these sectors employed increasing numbers of non-permanent residents even prior to 2022.

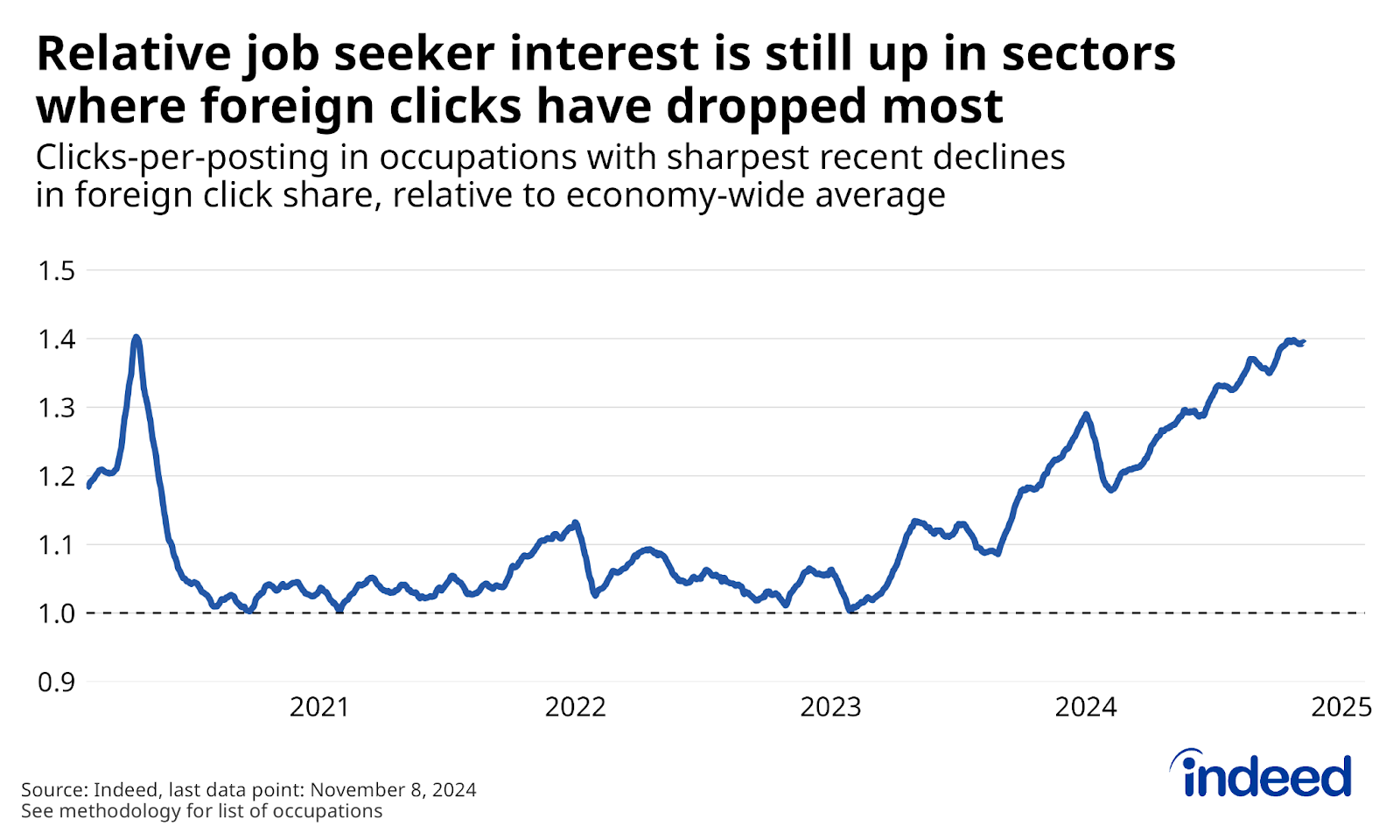

But while the decline in foreign job seeker interest signals a change in where employers may find their next candidate, there’s little sign it’s gotten tougher for them to fill job openings. Taken together, job postings for the occupations that experienced the sharpest drops in foreign click share since mid-2023 — such as driving, personal care and home health, retail, and cleaning and sanitation — experienced increased relative job seeker interest over the same period, despite less interest from abroad (i.e. their clicks-per-posting rose relative to the economy-wide average). This suggests that amid ongoing labour market weakness, domestic job seekers will likely offset some of the hiring challenges employers might face from new arrivals to Canada.

Instead of falling population inflows, the bigger wild card for the labour market in 2025 is the potential effects from rising outflows of non-permanent residents as work and study visas expire. The impact of these departures are abound with uncertainty, as there is limited up-to-date labour market data tracking non-permanent residents1 and because the ultimate number of people that will leave is up in the air.

That said, these outflows will surely cause some disruption in the labour market. In lower-paying sectors with high employee turnover, the impacts might be relatively muted in regions where employer demand is currently weak — including Toronto and other cities in southern Ontario. However, employers might have to make greater adjustments in regions where job postings have held up better, including rural areas. At the same time, non-permanent residents, many of whom are in Canada on post-graduate work permits, are employed in jobs across the economy. There will likely be many cases where expiring work visas cause challenges for business operations, not to mention for the workers themselves.

Wage growth could cool after a strong 2024

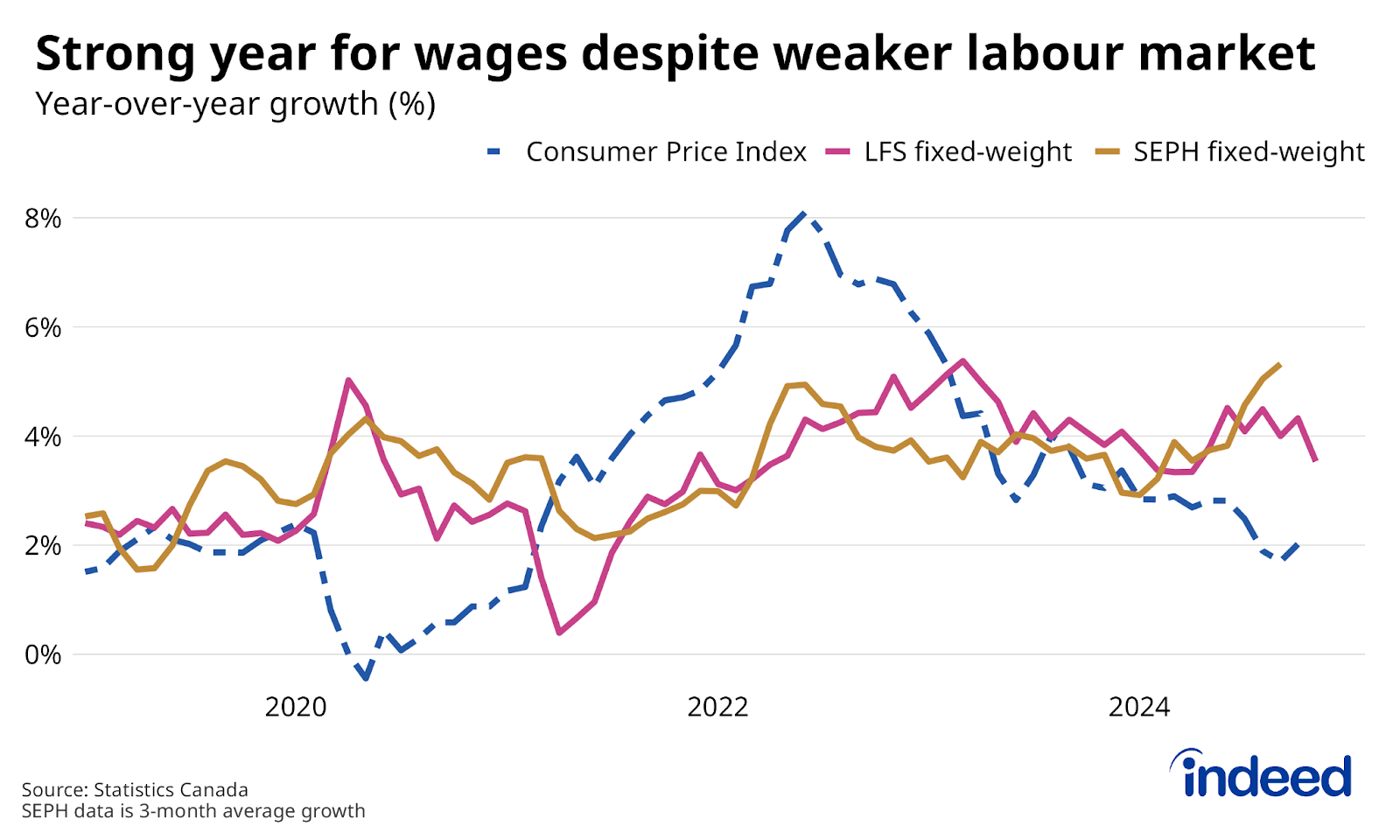

Rising unemployment, falling job vacancies, and easing inflation suggested wage growth would slow in 2024. However, throughout the year, hourly earnings, as measured by the LFS and the Survey of Employment Payrolls and Hours (SEPH), continued to rise at a brisk pace. After adjusting for changing jobs-mix, wages in the LFS grew at around a 4% year-over-year pace for much of 2024, while pay gains in SEPH accelerated to over 5% during the third quarter. Wages also outpaced price growth, with inflation easing to 2% by October, and there were few signs that higher labour costs translated to materially higher prices at the aggregate level.

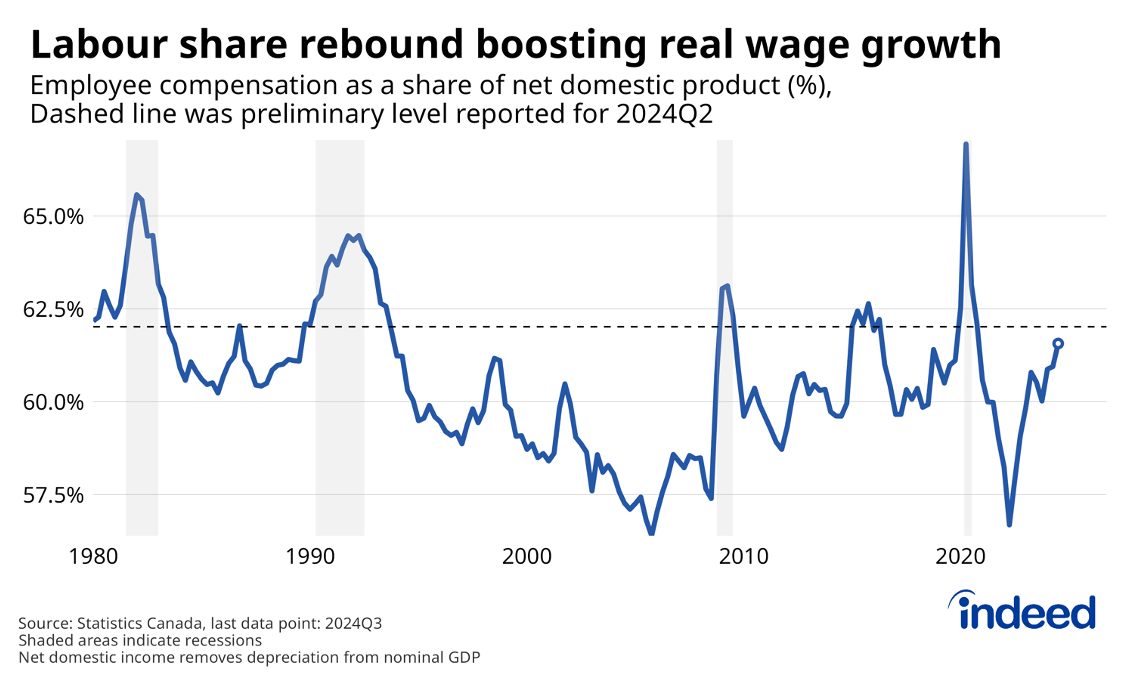

Meanwhile, productivity — a key driver of real (inflation-adjusted) wages — continued to decline. Real wages rose despite falling output per hour worked, because the labour share of national income rebounded further from its low point during the 2022 surge in inflation. A combination of cost-of-living pay increases and perhaps the lingering effects from earlier labour market tightness appears to have helped paychecks to catch up to the surge in business profits that accompanied the earlier jump in prices.

Room for this catch-up process appeared to be dwindling by early 2024, but recent upward revisions to Canadian GDP growth between 2021 and 2023 meant the labour share of net domestic product wasn’t as elevated as initially reported. Nonetheless, history suggests that real compensation growth and productivity growth can only diverge for so long. As of Q3 2024, the labour share had reached levels rarely seen outside of recessionary periods, which could mean a slowdown in wage growth is coming.

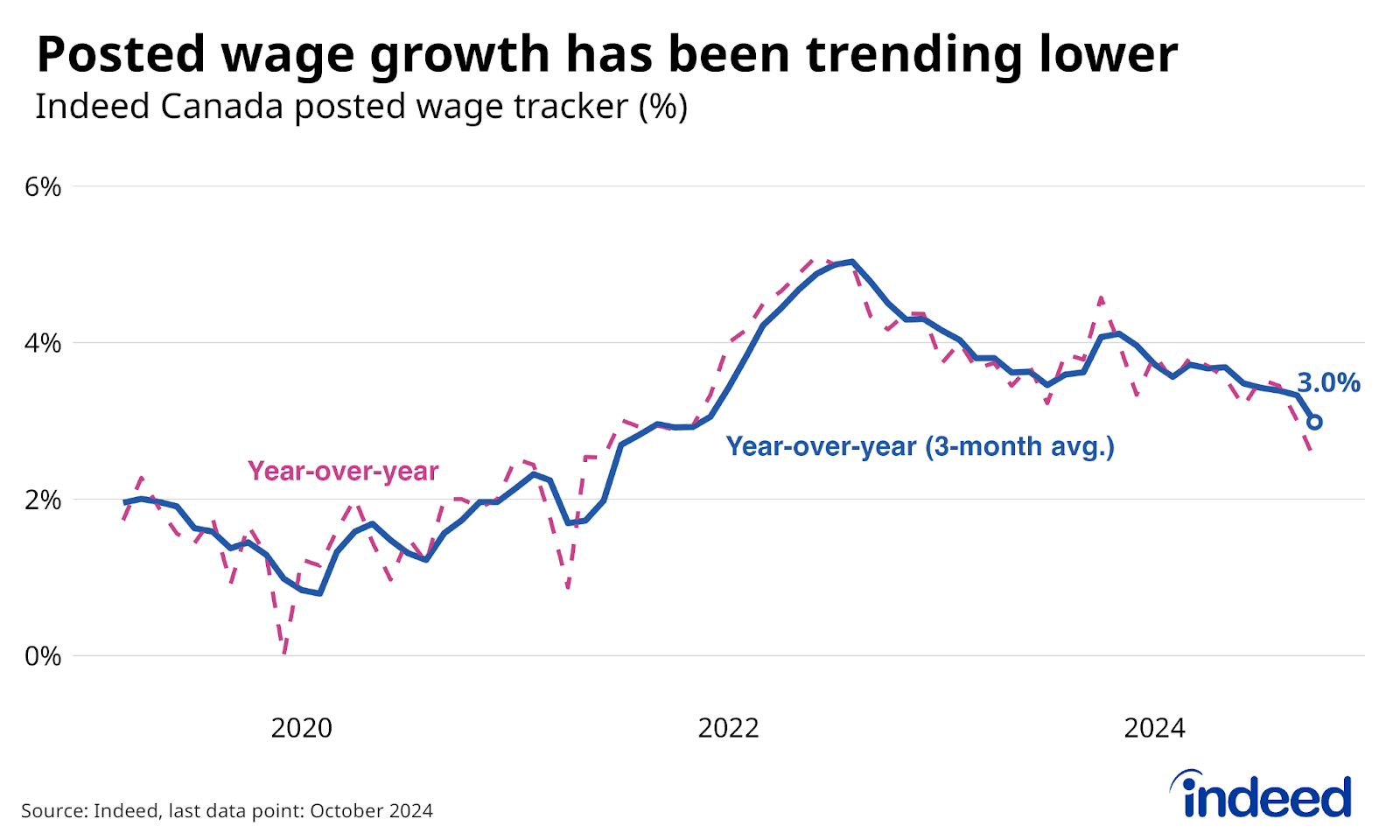

There are already signs that wage growth is easing. Headline hourly pay in the November LFS rose at its slowest year-over-year pace since 2022. While one month is too soon to declare a trend, employers on Indeed have also recently been less aggressive in the wages and salaries they post that are meant to attract job seekers. Year-over-year growth in the Indeed Wage Tracker averaged 3.0% over the three months through October, its slowest pace since late 2021. If slower growth for offered wages translates into the paychecks of new hires, it’s a likely sign of where the broader labour market is heading.

While economy-wide wage growth might cool, there’s also potential for different dynamics across different occupations and sectors. One factor could be further strength in public sector wage growth as collective bargaining agreements reset. Despite picking up in 2024, wage growth among public sector employees has lagged private sector employees since 2022.

Meanwhile, the government’s immigration policy changes could also impact the distribution of wage growth. The LFS and SEPH show different patterns in how wages of lower-paying occupations/industries have fared compared to the economy-wide average since Canada’s population surge began in 2021.2 However, neither survey suggests the same degree of pandemic-era wage compression seen in the US, and Canada’s rapid growth in non-permanent residents could be one reason why.3 If the ranks of non-permanent residents drop in 2025, there could be greater pressure on employers in lower-paying sectors to hike wages to attract workers, though it remains to be seen if broader economic conditions will necessitate it.

Generative AI is changing tech jobs, but rarely mentioned in other job postings

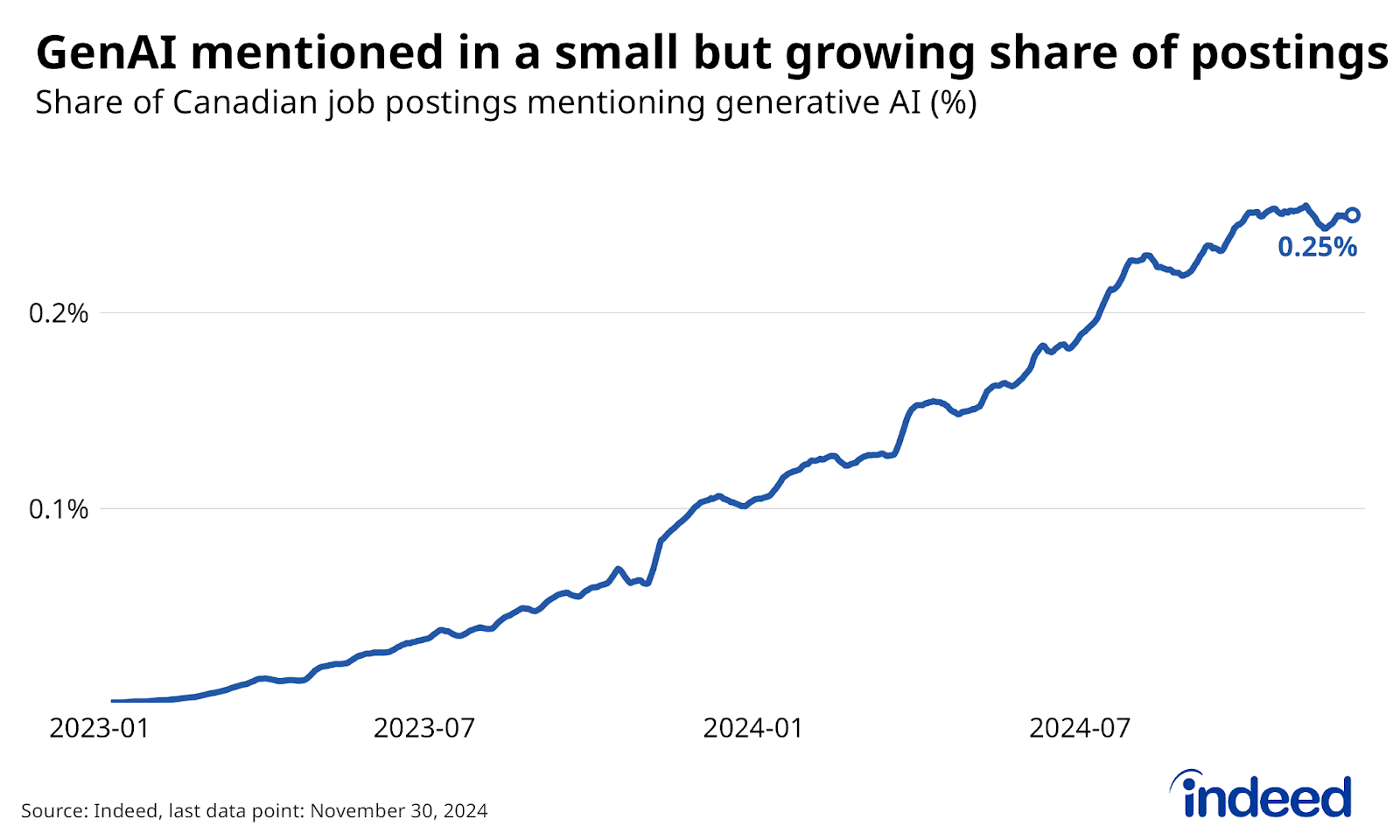

Roughly two years since the introduction of ChatGPT and other generative artificial intelligence (GenAI) models, usage of GenAI tools continues to grow throughout the labour market, though their application is far from ubiquitous. As of the third quarter of 2024, 10.6% of Canadian businesses said they’d be using some form of artificial intelligence to deliver products and services over the next year, surely higher than years prior, but still a minority of firms. A similar trend is evident in job postings. In November 2024, 0.25% of job postings explicitly mentioned any of a basket of GenAI-related terms in their descriptions, more than double the 0.09% share from a year earlier, but a small overall presence.

So far, mentions of GenAI are primarily found in tech-related job postings. In late 2024, GenAI was mentioned in 2.4% of job postings in fields including software development and mathematics, a sizable presence given how new the technology is. But, outside these fields, the share was just 0.1% of postings. This suggests that despite the potential application of GenAI across wide areas of the labour market, its adoption remains relatively limited outside of the tech sector. Nonetheless, while scaling up the use of cutting-edge technologies has historically been a challenge in the Canadian economy, the steady growth in postings mentioning GenAI highlights how the trend remains in its early stages.

Summing up

The job seeker’s market that emerged in the wake of the pandemic has steadily eroded over the past two years, and a turnaround will require a break from current economic trends. A few factors on the horizon could, in fact, change the situation: The drag from earlier Bank of Canada rate hikes will likely start waning, while slower population growth will mean fewer people entering an already struggling labour market (though rising outflows of non-permanent residents will also cause disruption). At the same time, a potential upheaval to Canada-US trade adds a new dose of uncertainty that won’t help near-term prospects. This could mean more of the same to kick off 2025, including a challenging environment for job seekers overall, though not one without opportunities for those in the right regions and occupations.

1Public LFS data doesn’t provide any information on the types of jobs non-permanent residents work in (and potentially undercounts their ranks), while the most recent alternative data published by Statistics Canada is from 2021.

2Since 2021, hourly wages of low-wage private sector occupations in the LFS have grown slower than average, but low-paying industries in SEPH have grown similarly to the headline trend.

3 Canada’s lack of “Great Resignation” is another potential factor.

Methodology

All job postings figures in this blog post are the index of seasonally adjusted Canadian job postings on Indeed re-based to February 1, 2020, using a seven-day trailing average.

The number of job postings on Indeed, whether related to paid or unpaid job solicitations, is not indicative of potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.

Occupations including when calculating relative job seeker interest among sectors where foreign clicks have dropped most include: Childcare, Security and Public Safety, Retail, Loading and Stocking, Driving, Cleaning and Sanitation, Personal Care and Home Health, and Construction.

To calculate fixed-weight wage growth in the LFS, we bucket LFS microdata for each of the 43 occupation groups into three levels of job tenure (6 months or less, 7 to 24 months, and 25 months and over), and recalculate headline average wages into a composition-adjusted measure by holding their respective weights constant at February 2020 levels.